Even before the COVID-19 pandemic, women were shortchanged in retirement.

Getty Images/iStockphotoAccording to the National Retail Federation, Mother’s Day spending is expected to total a record $28.1 billion this year, up $1.4 billion from last year. Can you imagine if instead of splurging on flowers and gifts, that much money were to pour into women’s retirement accounts this month?

Of course, that’s not going to happen. We all love to pamper the moms in our lives on their special day with bouquets and other gifts. And from a practical standpoint, many in the workforce don’t even have a retirement account in which to deposit retirement savings.

But there is one thing we all can do on Mother’s Day – commit to finding solutions that deliver better retirement security for women.

Many Americans are struggling to save for retirement, but women face even higher hurdles. The causes include the gender pay gap, longer life spans, and greater caregiving responsibilities.

The economic outlook for women has worsened due to the COVID-19 pandemic. More than 2.3 million women have left the workforce since February 2020, with female workforce participation dropping to 57%, the lowest level since 1988.[1] Over time, this likely will translate to a worsening of women’s retirement wealth gap.

Even before the COVID-19 pandemic, women were shortchanged in retirement. Older women receive about 80% of the retirement income older men receive, a disparity that mirrors the gender pay gap. More specifically, women age 65 and older had a median household retirement income of $47,244 in 2016, which is 83 percent of median household income for men, at $57,144.[2]

MORE FOR YOU

Given their lower savings levels and the plethora of economic challenges women face, it’s not surprising that compared to men, women are more concerned about retirement. In December 2020, the National Institute on Retirement Security polled working age Americans on their views on retirement. We took a closer look at the sentiment of women and we found that women indeed are more concerned about retirement than men.

More specifically:

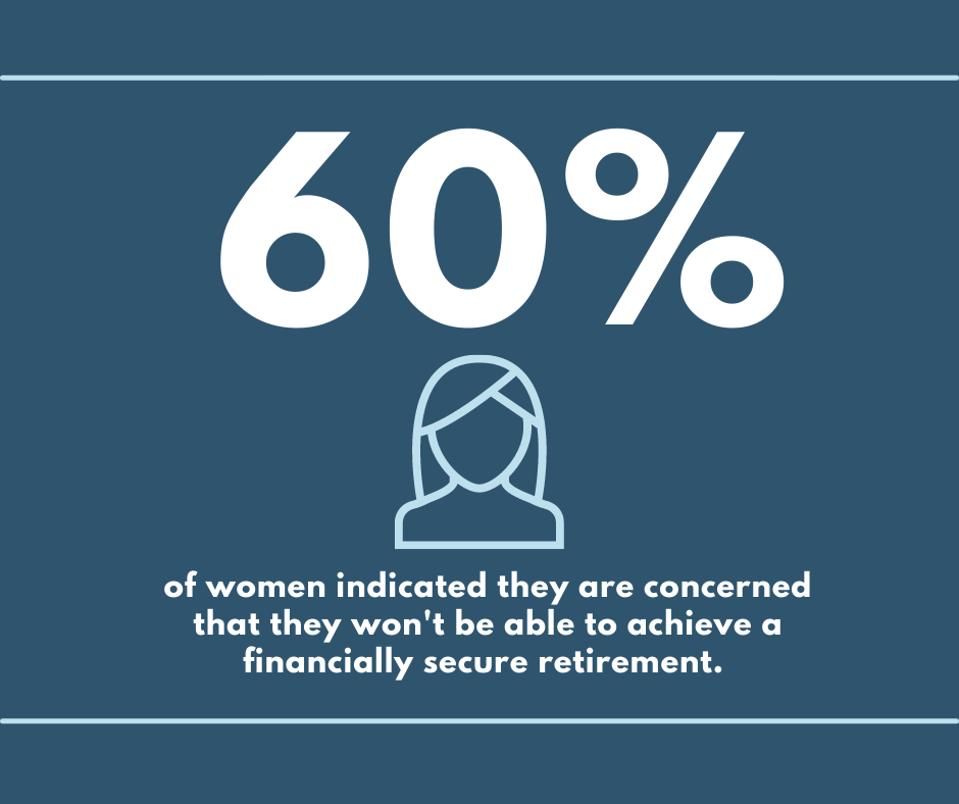

— 60% of women indicated they are concerned that they won't be able to achieve a financially secure retirement, with 30 percent very concerned. By comparison, 51% of men are concerned.

Women are worried about retirement.

National Institute on Retirement Security— Nearly three-fourths of women (71%) agree that the average worker cannot save enough on their own to guarantee a secure retirement. Men were at 65 percent.

— Nearly two-thirds of women (63%) say that it’s only getting harder to prepare for retirement in the future.

We also asked why retirement is getting harder. Women said the top two factors are the rising costs of healthcare and long-term care. This isn’t surprising given that women live longer than men, which means they are more likely to face higher healthcare and long-term care costs in their retirement years. Other major factors were wages not keeping up, a lack of pensions, longer life spans, increasing debt, and do-it-yourself retirement plans.

But what can be done to improve women’s economic security in their older years? The problem seems daunting, especially if women and families try to take steps without help. The more effective approach would be for policymakers to enact solutions that update features of the retirement savings infrastructure to meet the needs of women in the 21st century.

Policymakers can take action to improve women's retirement outlook.

Getty Images/iStockphotoFor example, as Congress considers whether and how to expand Social Security, adjusting the spousal benefit and providing caregiving credits in Social Security would make a substantial difference for women. Also, states could adopt better family leave policies to make it less punitive for women to take time out of the labor force to provide caregiving.

Also, both Congress and state legislatures could consider permanently removing age limits on the Earned Income Tax Credit (EITC), so that low-income women all of ages could receive this income boost. Finally, creating a universal savings vehicle for all women, including those in caregiving roles, would give working women the opportunity to save for their retirement even if their employer does not offer a plan.

For certain, the problem of the retirement wealth gap won’t be solved overnight. But we all owe it to the moms in our lives to make women’s retirement security a top priority on Mother’s Day and every day.

[1] National Women’s Law Center, Another 275,000 Women Left the Labor Force in January, February 2021.

[2] National Institute on Retirement Security, Still Short-Changed, May 2020.

The Link LonkMay 08, 2021 at 01:52AM

https://www.forbes.com/sites/dandoonan/2021/05/07/for-mothers-day-forget-the-flowers-and-get-retirement-security-for-moms/

For Mother's Day, Forget The Flowers And Get Retirement Security For Moms - Forbes

https://news.google.com/search?q=forget&hl=en-US&gl=US&ceid=US:en

No comments:

Post a Comment